Should You Buy Property with Loan in 2026?

Buying property is one of the biggest financial decisions most people make in life.

For many Indians, owning a home represents:

- financial security,

- social stability,

- long-term investment,

- and emotional satisfaction.

However, with rising:

- property prices,

- home loan interest rates,

- construction costs,

- and changing market trends,

many people are asking an important question:

Should you buy property with loan in 2026?

The answer depends on:

- your financial condition,

- market timing,

- loan eligibility,

- investment goals,

- and repayment capacity.

In this complete guide, we will discuss:

- advantages of buying property with loan,

- risks involved,

- market trends in 2026,

- EMI planning,

- and smart financial strategies before purchasing property.

Why Property Ownership Still Matters

Despite market fluctuations, real estate remains one of the strongest long-term assets in India.

Property ownership provides:

- long-term security,

- inflation protection,

- wealth creation,

- and future financial stability.

Unlike rented accommodation:

- property ownership creates an asset,

- while loan repayment gradually builds equity.

Why Most People Buy Property Through Home Loan

Very few buyers purchase property entirely with cash.

Most people use home loans because:

- property prices are high,

- loans make ownership affordable,

- repayment is spread over years,

- and tax benefits are available.

Home loans help buyers:

Own property without waiting decades to save full amount.

Real Estate Market Trends in 2026

The Indian real estate market continues evolving rapidly.

Key trends include:

- increasing urban housing demand,

- infrastructure growth,

- smart city expansion,

- rising construction costs,

- and digital property transactions.

Tier-2 cities like:

- Agra,

- Lucknow,

- Jaipur,

- Indore,

- and Chandigarh

are also seeing strong growth due to:

- lower property costs,

- better connectivity,

- and rising employment opportunities.

Is 2026 a Good Time to Buy Property?

For many buyers:

Yes, 2026 can be a strong opportunity.

Especially for:

- long-term homeowners,

- stable salaried professionals,

- business owners,

- and investors with disciplined financial planning.

However, the decision should depend on:

- affordability,

- financial stability,

- and long-term goals.

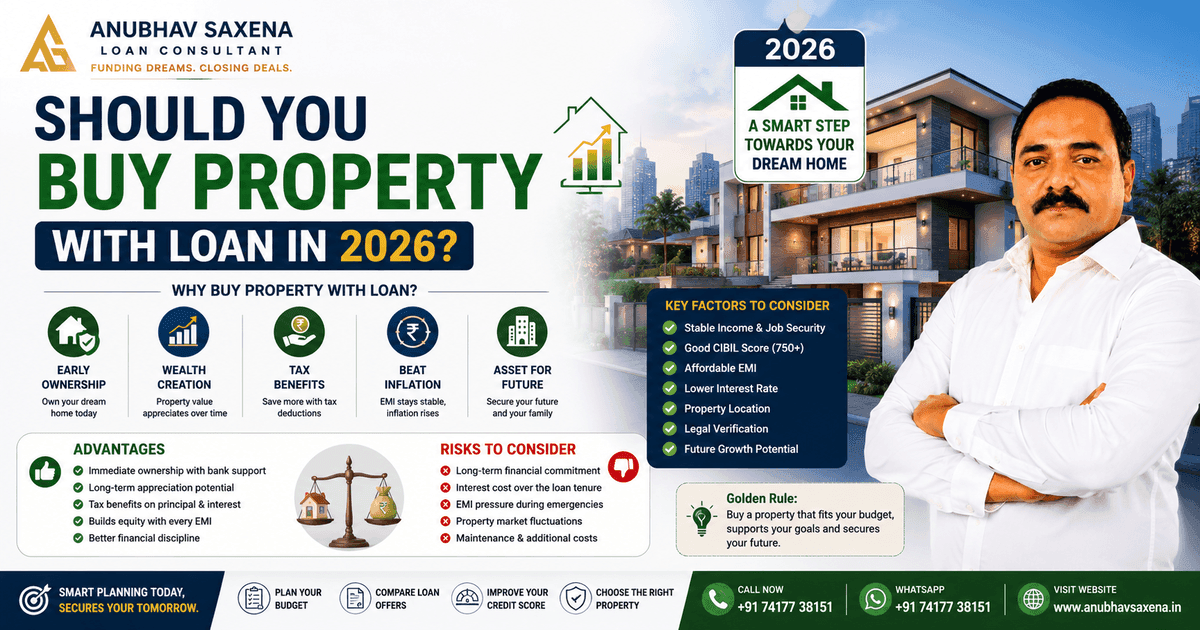

Advantages of Buying Property with Loan

1. Early Property Ownership

Home loans allow buyers to own property much earlier.

Without loans:

- many people may spend decades saving money.

With financing:

- ownership becomes immediately possible.

2. Property Value Appreciation

Real estate values generally appreciate over time.

Buying property early may help benefit from:

- future price growth,

- infrastructure development,

- and urban expansion.

Example

A property purchased today may become significantly more valuable after:

5–10 years

depending on location and development.

3. Tax Benefits on Home Loan

Home loans offer important tax benefits in India.

Borrowers may claim deductions on:

- principal repayment,

- and home loan interest.

This reduces overall tax burden.

4. Inflation Advantage

Over time:

- salaries may increase,

- rental costs rise,

- but EMI may remain relatively stable.

This makes long-term loan repayment easier compared to future property prices.

5. Asset Creation

Unlike rent payments:

Home loan EMIs gradually create ownership.

Each EMI increases your property equity.

6. Financial Discipline

Home loans encourage:

- savings discipline,

- income planning,

- and long-term financial responsibility.

Risks of Buying Property with Loan

While there are advantages, buyers should also understand risks.

1. Long-Term Financial Commitment

Home loans usually continue for:

15–30 years

This becomes a major financial responsibility.

2. Interest Cost

Borrowers pay:

- principal amount,

- plus interest over years.

Longer tenure increases total interest paid.

3. EMI Pressure

High EMI burden can create:

- financial stress,

- reduced savings,

- and lifestyle pressure.

Especially during:

- job loss,

- business slowdown,

- or emergencies.

4. Property Market Risk

Property prices may not always rise quickly.

Poor location selection can reduce investment returns.

5. Maintenance Costs

Property ownership also includes:

- maintenance,

- repairs,

- taxes,

- and society charges.

These additional costs must be considered.

Should You Buy Property for Living or Investment?

This is extremely important.

Buying for Self-Use

If you need:

- long-term residence,

- family stability,

- and personal ownership,

then buying property may be emotionally and financially valuable.

Buying for Investment

Investment-focused buyers should evaluate:

- rental yield,

- future appreciation,

- location growth,

- and liquidity.

Not every property becomes a profitable investment.

Important Factors Before Buying Property in 2026

1. Financial Stability

Before taking home loan:

- income should be stable,

- emergency savings should exist,

- and EMI affordability should be comfortable.

Ideal EMI Rule

Experts generally recommend:

EMI should remain manageable

compared to monthly income.

2. Down Payment Capacity

Higher down payment reduces:

- loan burden,

- EMI pressure,

- and interest cost.

3. Credit Score

Healthy CIBIL score improves:

- approval chances,

- interest rates,

- and loan flexibility.

Most banks prefer:

750+

for smooth processing.

4. Loan Interest Rate

Even small interest differences matter significantly over long tenures.

Compare:

- banks,

- NBFCs,

- and loan schemes carefully.

5. Property Location

Location strongly affects:

- appreciation,

- rental demand,

- resale value,

- and future growth.

Good infrastructure areas usually perform better.

6. Legal Verification

Always verify:

- title deed,

- approvals,

- RERA registration,

- and property legality.

Legal issues can create major financial problems later.

Ready-to-Move vs Under-Construction Property

Ready-to-Move Property

Advantages:

- immediate possession,

- lower uncertainty,

- easier verification.

Disadvantages:

- higher prices,

- limited customization.

Under-Construction Property

Advantages:

- lower initial pricing,

- flexible payment plans.

Disadvantages:

- construction delays,

- project risks,

- approval issues.

Fixed vs Floating Interest Rate

Fixed Interest Rate

- EMI remains stable,

- predictable repayment,

- less uncertainty.

Floating Interest Rate

- interest changes with market conditions,

- EMI may rise or fall,

- potentially lower long-term cost.

Choice depends on:

- financial stability,

- risk tolerance,

- and market expectations.

Should Salaried Employees Buy Property in 2026?

For salaried professionals:

Stable income improves home buying confidence.

Good candidates include:

- stable employment,

- healthy savings,

- manageable debt,

- and long-term residential goals.

Should Business Owners Buy Property in 2026?

Business owners should evaluate:

- cash flow stability,

- business growth,

- and market uncertainty carefully.

Business income fluctuations can impact EMI management.

Is Renting Better Than Buying?

This depends on:

- lifestyle,

- financial goals,

- and location.

Renting Advantages

- flexibility,

- lower upfront cost,

- easier relocation.

Buying Advantages

- asset creation,

- ownership,

- long-term stability,

- and appreciation potential.

Common Mistakes Buyers Make

Buying Beyond Budget

Oversized loans create financial pressure.

Ignoring Emergency Savings

Many buyers exhaust all savings in down payment.

Not Comparing Loan Offers

Different lenders provide different terms.

Ignoring Property Legal Checks

Legal verification is extremely important.

Choosing Wrong Location

Poor location affects future value and resale.

How to Buy Property Smartly in 2026

Improve Credit Score Early

Healthy score improves loan terms.

Compare Multiple Lenders

Do not accept first offer blindly.

Keep Proper Emergency Fund

Financial safety is extremely important.

Choose Affordable EMI

Avoid stretching budget excessively.

Think Long-Term

Property should align with:

- future family goals,

- career plans,

- and financial stability.

Frequently Asked Questions

Is 2026 a good year to buy property?

For financially stable buyers:

Yes, long-term opportunities remain strong.

Is home loan better than paying rent?

It depends on:

- affordability,

- location,

- and long-term plans.

How much down payment is ideal?

Higher down payment reduces:

- EMI,

- loan burden,

- and interest cost.

What credit score is needed for home loan?

Most banks prefer:

750 or above

Is property a good long-term investment?

In strong locations:

Real estate can create long-term wealth.

Final Thoughts

Buying property with loan in 2026 can be a smart financial decision if:

- your income is stable,

- EMI is affordable,

- financial planning is strong,

- and property selection is correct.

Home ownership provides:

- security,

- stability,

- and long-term wealth creation.

However, buyers should avoid:

- emotional decisions,

- excessive debt,

- and poor financial planning.

The best property purchase is one that:

Improves your future without damaging your financial stability.

With proper planning, home loans can become a powerful tool for:

- asset creation,

- financial growth,

- and long-term security.

Need Home Loan or Property Finance Guidance?

Anubhav Saxena provides expert support for:

- Home Loans

- Property Finance

- Business Loans

- Project Finance

- Agriculture Loans

- CC Limit & OD Limit

Get professional help for:

- loan eligibility,

- documentation,

- property finance planning,

- and faster approvals.

Funding Dreams. Closing Deals.